Pareto validation

During my university years and a little bit after, I was involved in the VC and startup scene where I lived. Especially during university, I was the president of a student association for tech entrepreneurship, I got to meet a lot of investors. I spent time in incubators and accelerators. Talking to founders about raising money and witnessing some seed and series A rounds was part of my routine.

One of the things that struck me most was how VCs - venture capitalists and investment funds - rely heavily on second-order observations. Here’s what I mean: Typically, there’s a lead investor who provides a significant portion of the funding. Other investors may contribute smaller amounts. While these smaller checks don’t mean much by themselves, they add up. When a big-name VC invests, it creates a ripple effect. Others follow because “if X invested, there must be something worth investing in. These big players are seen as having done their homework. It’s a generalization, sure, but one that’s easy to see in headlines and trends. Just think about how many funds have started investing in AI en masse since 2020-2021.

Isn’t that how we all operate, even in our personal lives? We take our cues from friends, listen to experts, and often skip our own due diligence. It’s a form of mimicry, doing what others tell us to do. It would be overwhelming to question every decision thoroughly.

I assumed VCs would be more methodical, given the large amounts of money involved. I thought they would follow a strict investment thesis and process. They would believe in a future trend and see if startups were aligned with that vision. But it seems that this mimicry is prevalent in many areas, not just VCs. To expect anything different may be naive.

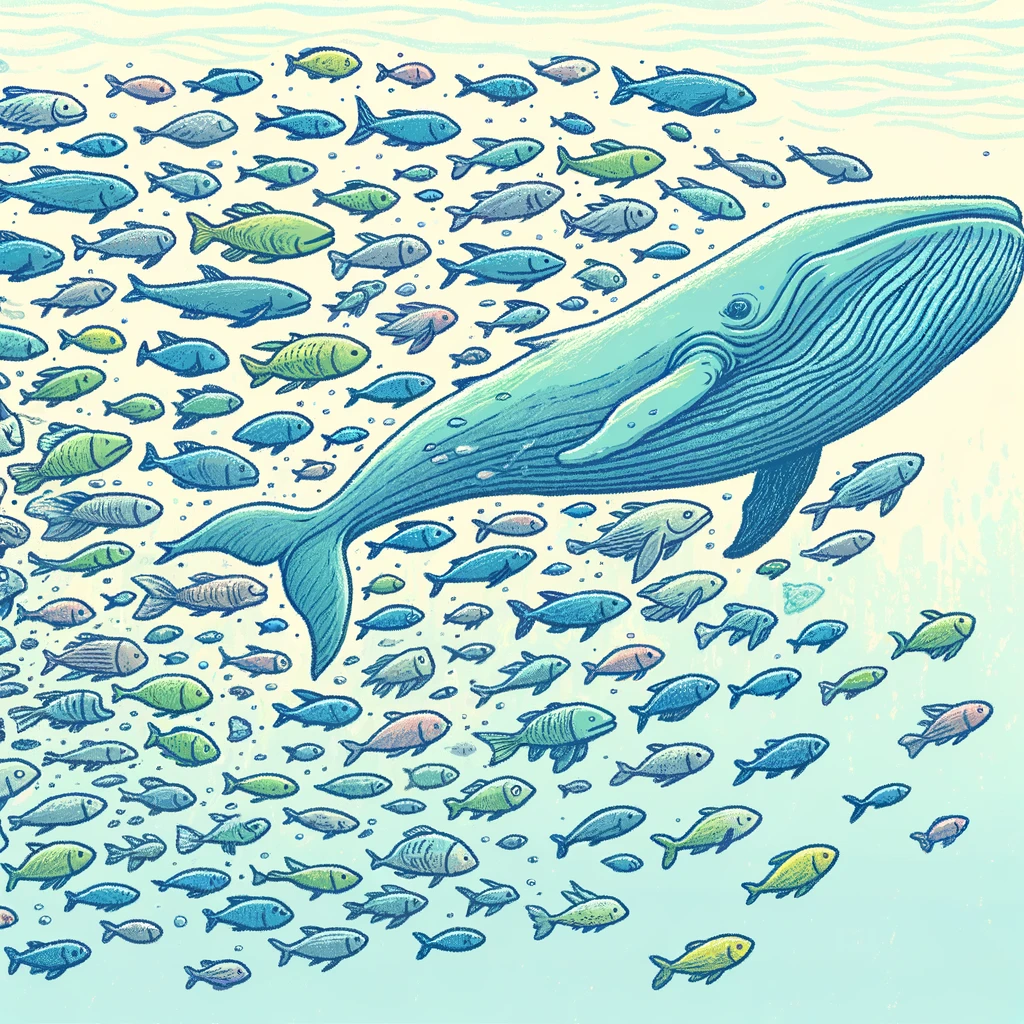

This brings to mind the Pareto Principle, where 80% of the effects come from 20% of the causes. In this case, we have a similar situation where 80% of VCs follow the 20% of the most successful VCs. It could be even more skewed. This is similar to the rise of copy trading in the financial world over the last five years, where investors simply mirror the trades of those they follow.

It’s not necessarily wrong; it makes sense. But it suggests a lot of inefficiency. When everyone is following the “big fish,” some opportunities are missed. These missed opportunities could be ripe for first-principle or contrarian investing - steering clear of crowded areas to find less obvious, but promising, opportunities.

I recently found a website listing industries by TAM (total addressable market) and capital invested. As an overlooked industry example, the petrochemical market has a TAM of 700 billion, but only 93 million invested per year. How many examples like this are out there?

I wonder if this pattern of behavior extends beyond investing to other aspects of life. The tendency to follow leads without deep investigation may be a common thread. But in the startup and VC world, where innovation and unique value propositions are prized, it’s curious that investment strategies often boil down to following the crowd.

Perhaps there’s room for a more principled approach that could uncover hidden gems that the crowd has overlooked. This idea, which I’ve come to call “Pareto validation,” suggests that sometimes the best path forward may be the one less traveled, guided by independent analysis rather than the movements of the crowd.